The U.S. solar industry grew 43% and installed a record 19.2 gigawatts (GWdc) of capacity in 2020, according to the U.S. Solar Market Insight 2020 Year-in-Review report, released today by the Solar Energy Industries Association (SEIA) and Wood Mackenzie.

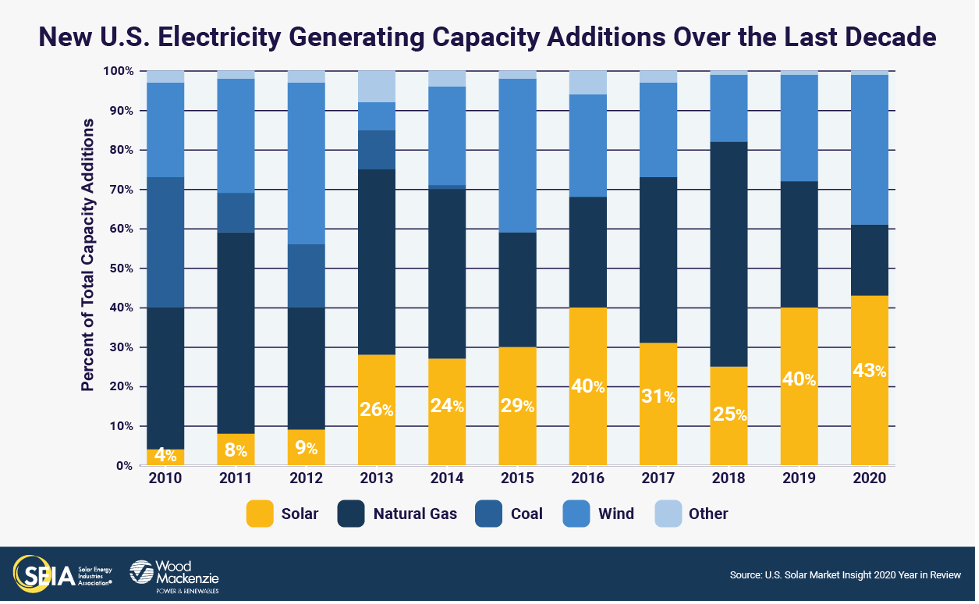

For the second year in a row, solar led all technologies in new electric-generating capacity added, accounting for 43%. According to Wood Mackenzie’s 10-year forecast, the U.S. solar industry will install a cumulative 324 GWdc of new capacity to reach a total of 419 GWdc over the next decade.

The 8 GWdc of new installations in Q4 2020 marks the largest quarter in U.S. solar history. For perspective, the U.S. solar market added 7.5 GWdc of new capacity in all of 2015. New capacity additions in 2020 represent a 43% increase from 2019 and breaks the U.S. solar market’s previous record of 15.1 GWdc set in 2016.

“After a slowdown in Q2 due to the pandemic, the solar industry innovated and came roaring back to continue our trajectory as America’s leading source of new energy,” said SEIA president and CEO Abigail Ross Hopper.

This is the first time Wood Mackenzie has released a long-term forecast (see below) as part of the U.S. Solar Market Insight report series. By 2030, Wood Mackenzie is forecasting that the total operating solar fleet will more than quadruple.

“The forecast shows that by 2030, the equivalent of one in eight American homes will have solar, but we still have a long way to go if we want to reach our goals in the Solar+ Decade. This report makes it clear that smart policies work. The action we take now will determine the pace of our growth and whether we use solar to fuel our economy and meet this climate moment,” added Hopper

“The recent two-year extension of the investment tax credit (ITC) will drive greater solar adoption through 2025,” said Michelle Davis, senior analyst from Wood Mackenzie. “Compelling economics for distributed and utility-scale solar along with decarbonization commitments from numerous stakeholders will result in a landmark installation rate of over 50 GWdc by the end of the decade.”

California, Texas and Florida are the top three states for annual solar capacity additions for the second straight year, and Virginia joins them as a fourth state installing over 1 GWdc of solar PV. In 2020, 27 states installed over 100 MWdc of new solar capacity, a new record.

Key findings:

- Residential deployment was up 11% from 2019, reaching a record 3.1 GW. This was lower than the 18% annual growth in 2019, as residential installations were significantly impacted by the pandemic in the first half of 2020.

- Non-residential installations declined 4% from 2019, with 2 GW installed. The pandemic impacted this segment through delayed project interconnections and prolonged development timelines.

- There was a historic 6.3 GWdc of utility-scale projects installed in Q4 2020, bringing the annual total just shy of 14 GWdc.

- A total of 5 GWdc of new utility solar power purchase agreements were announced in Q4 2020, bringing the volume of project announcements in 2020 to 30.6 GWdc and the full utility-scale contracted pipeline to 69 GWdc.

- The 2-year extension of the ITC in the final days of 2020 has led to a 17% increase in deployment in our 2021 – 2025 forecast.

{kind=link}